The Petroleum Hub

It has long been the dream of many West African countries including Nigeria, Ivory Coast, Togo, Ghana and Burkina Faso to create a physical downstream petroleum hub; a geographical (centrally located and sufficiently inter-connected) point in the network where a price is set for petroleum products delivered at the specific location.

This project is largely meant to meet the petroleum demand of local and sub-regional economy, and possibly to satisfy demand on a continental scale.

But beyond the demand factor, the hub creation is expected to accelerate growth in the downstream sector, and to position it as a key player in an economy. It is also envisaged that it would generate foreign direct investment (FDI), create employment, grow knowledge transfer, attract major international trading firms, stimulate mergers and joint ventures, deepen the linkage between the upstream and downstream sectors of the petroleum industry, and most especially; to create economic value.

In Ghana, the hope is to create a petroleum hub for the downstream sector to grow the country’s gross domestic product (GDP) by 70 percent by 2038, provide millions of jobs, and to store and distribute 50 percent of West Africa’s petroleum product demand. This vision was further advanced in 2018 with the announcement of growing its refinery capacity from a paltry 45,000 barrels per stream day (bpsd) to over 600,000 bpsd by building four new refineries. Storage, vessel berths and pipeline capacities are equally expected to be increased to accommodate the movement of crude oil and clean products.

The Government of Ghana (GoG) is currently courting the private sector to commit to 90 percent funding of the total $50 billion project cost, meaning the project is expected to be private sector driven.

Products Demand in West Africa

Africa’s consumption of petroleum products have been increasing at an annual average rate of more than 3% since the last decade. This growth in consumption continue to be largely influenced by urbanization, rising population, and strong gross domestic product (GDP) growth.

In sub-Saharan Africa (SSA), the total oil products consumed in 2017 stood at 99.5 million metric tonnes (mmt), whereas West and Central Africa (WCA) consumed 46.1mmt as reported by CITAC, an energy research body. It is also reported that in 2017 Nigeria, Angola and Ghana retained their position as the three top clean products demand centers in WCA; consuming 19.15mmt, 5.1mmt, and 3.72mmt respectively. On the part of the International Monetary Fund (IMF), it expected refined product demand to experience an average growth rate for SSA of 3.4% in 2018, with the figure expected to rise to almost 4.1% by 2030.

In spite of these high demands, SSA is largely reliant on imported refined products to meet its fast growing petroleum demand, as a result of the low refinery capacity and utilization rate, causing persistent fuel shortage in especially Nigeria and Angola each year. CITAC reports that refined products shortfall (the difference between refinery output and demand) is expected to rise to over 150mmt per year by 2030, up from 79mmt in 2015; resulting in ever increasing requirements for fuel imports in SSA.

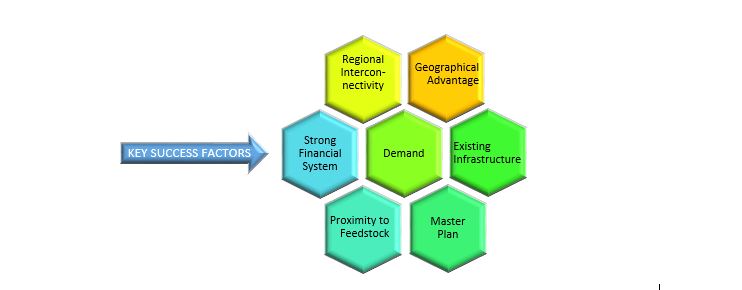

Critical Success Factors (CSFs)

It is clearly evident that a huge market opportunity exist to warrant the creation of a petroleum hub in the West and Central Africa sub-regions, and Ghana intends to take up the challenge.

However, any intention to build a petro-chemical hub must first and foremost be founded on market demand, with meeting domestic demand being the principal prerequisite. Targeting a regional market becomes imperative when the domestic demand is not adequate to warrant the creation of the hub.

In Ghana, the current daily consumption of approximately 80,000 barrels per day (10,800mt/d) compared to its refining utilization capacity of less than 28,000 barrels per day, makes a good case to expand its refinery capacity. Also West Africa’s growing demand of over 850,000 barrels per day, and imports from Europe and the Americas presents a much better case to develop a central clean product market in the sub-region.

But aside the demand factor, there are equally some key ingredients that Ghana must consider and take advantage of, to guarantee the successful and viable development of the petroleum hub. These other factors which are drawn from international experience (like the Amsterdam-Rotterdam-Antwerp petroleum hub in Europe) includes but may not be limited to geographical advantage, regional

interconnectivity, existing petroleum infrastructure, proximity to feed-stock, Master Plan for securing investor confidence, a strong financial system, and adequate skill-set.

Geographical Advantage: The accessibility of the hub is key in facilitating the growth of the petroleum market in the region and on the international market.

Ghana is strategically located along the Atlantic Ocean and Gulf of Guinea, a key shipping corridor of Asia and Europe that connects the East and West globally. The geographical advantage allows Ghana to become an international petroleum hub, riding on increased vessel traffic along the corridor to attract vessels to call on ports of Ghana for storage, lifting, bunkering, and various dock activities. Also, Ghana’s coastline has relatively safe maritime domain, with water depth capable of accommodating very large ocean vessels.

Regional Interconnectivity: As the definition of a hub goes beyond building an activity geographically in a single location, it may comprise of diverse production and logistics sites that leverage on their strategic and natural superior position to generate a greater outcome. The case with which the petroleum products could be easily and economically accessed through ports and fuel transmission systems are crucial elements to consider in developing a hub.

Currently, it is only the West Africa Gas Pipeline (WAGP) which has advanced regional interconnectivity and integration in the sub-region. Additional efforts are required to improve on the connectivity so as to deepen the consumption of local

hey wouldn’t need to employ expatriates at an unfavorable cost.

All these elements are essential in securing investor confidence and helps in the framing of a Master Plan for the hub, to provoke a positive outcome of the project.

The success of Ghana’s plan to develop a petroleum hub to meet its local demand, and also on regional and continental scale, would be so much dependent on how the country takes advantage of the factors listed, including few others; in positioning itself as the preferred destination for the hub.

Written by Paa Kwasi Anamua Sakyi, Institute for Energy Security © 2019

The writer has over 22 years of experience in the technical and management areas of Oil and Gas Management, Banking and Finance, and Mechanical Engineering; working in both the Gold Mining and Oil sector. He is currently working as an Oil Trader, Consultant, and Policy Analyst in the global energy sector. He serves as a resource to many global energy research firms, including Argus Media.

Leave a Reply